Taxes in Zug, Schwyz, Zurich and Geneva

Where should you live to pay the lowest taxes in Switzerland: in the canton of Zug or Schwyz?

Great question!

The right answer reaches beyond the superficial nature of the question, by looking at district level, or even commune level.

For a random municipality in Zug and Schwyz, the chances are much greater that Zug will have the lowest taxes: on average, taxes are lowest in the canton of Zug.

However, the minimum is in Schwyz. This is because there is a great deal of variability between the communes of Canton Schwyz. The 6 communes with the lowest taxes in Switzerland are all in Schwyz.

These are the 3 communes in the district of Höfe (Freienbach, Wollerau, Feusisberg) plus 3 of the communes in the district of March. Only then come Baar (ZG) and Zug (ZG).

In fact, the differences are small enough that they don't fundamentally change the game.

But if you live in the city or canton of Zürich, it's well worth considering whether to move to Zug or Schwyz. For high earners, the differences can be close to 100k- a year.

Geneva is further away, but the stakes are even higher!

Let's look at the details of each tax: on income, dividend, wealth, companies, capital gains, 2nd/3rd pillar, inheritance...

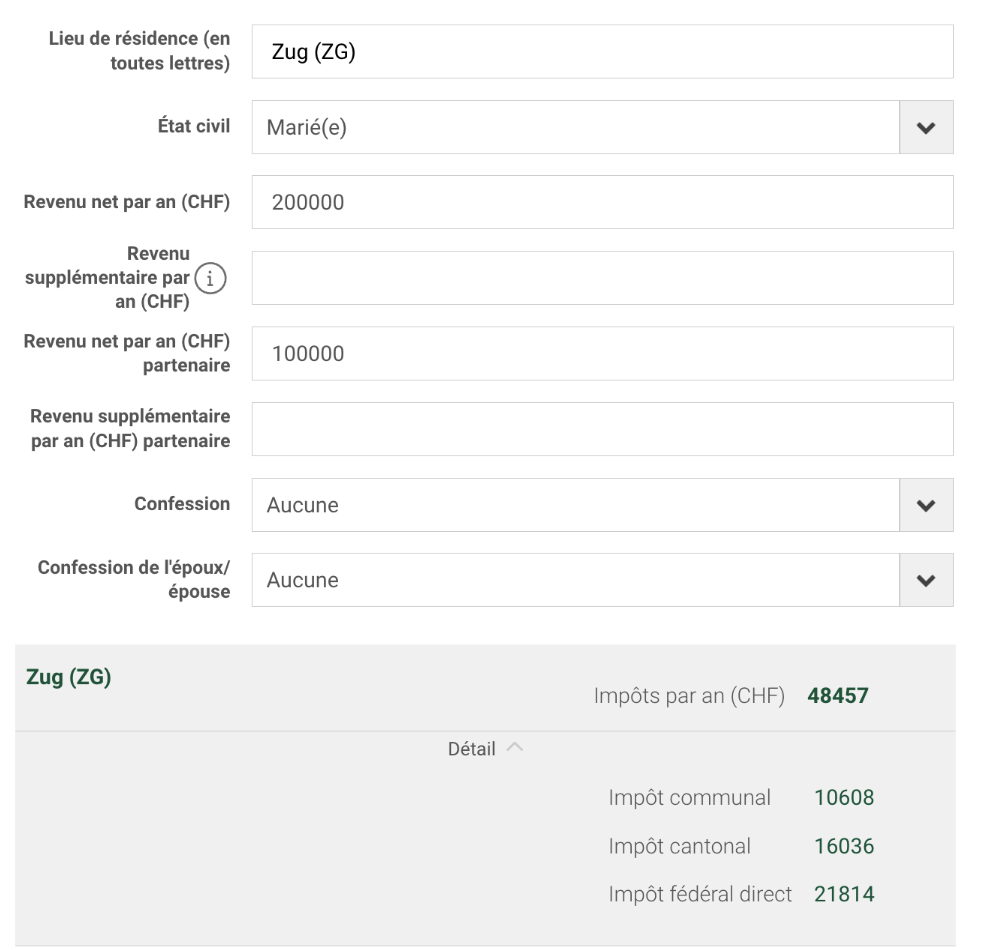

Income tax

Here are the tax figures for two couples in Höfe (SZ), Zug (ZG), Zürich (ZH) and Geneva (GE):

Source: comparis income tax calculator. Don't hesitate to use it yourself to assess your specific situation.

Dividend tax

It (almost) follows income tax.

Dividends are taxed on income (cantonal and communal) by a multiplication factor that depends solely on the canton: 50% for SZ, ZG and ZH and 70% for GE.

The differences are therefore small, and ZG has a slight advantage for dividends of 300k because ZG taxes smaller incomes more lightly than other cantons/municipalities.

Wealth tax

And here's the wealth tax amount for two couples:

Source: Vermoegenzentrum calculator.

Other attractive municipalities for wealth tax are NW, SZ, OW and UR - although there is little difference with SZ and ZG.

Feel free to use the calculator yourself to assess your specific case.

Corporate tax

Here are the corporate tax rates based on profits and capital. There is still little difference between Höfe (SZ) and Zug (ZG). Note the presence of Meggen (LU), which has the lowest tax rate on profits in Switzerland, and the cantons of UR and OW, which do not tax capital.

Source: Nexova comparison

Capital gains tax

In Switzerland, regardless of canton or municipality, there is no capital gains tax on private financial returns (e.g. on the sale of shares).

However real estate capital gains are taxed.

The rules vary according to the canton in which the property is located: in general, the amount of the tax depends on the amount of the capital gain and the length of time the property has been held: the higher the amount and the shorter the period, the higher the rate.

Under certain conditions, it is possible to defer this tax when selling to buy another property.

Here's the capital gains tax on a 1.5m- property, rising by 2.5% a year (as has been the case in Switzerland on average over the past 50 years):

| Capital gains tax on this property after |

5 years |

10 years |

15 years |

25 years |

|---|---|---|---|---|

| Höfe (SZ) & all of SZ |

50k- (25%) |

86k- (21.5%) | 105k- (17.5%) | 115k- (8.8%) |

| Zug (ZG) |

20k- (10%) |

40k- (10%) | 60k- (10%) | 130k- (10%) |

| Zürich (ZH) |

66k- (33%) |

120k- (30%) | 149k- (25%) | 255k- (20%) |

| Geneva (GE) |

60k- (30%) |

40k- (10%) | 60k- (10%) | 26k- (2%) |

Zug is almost always the winner. Only in the very long term does Geneva come out on top: it's similar to France where real estate capital gains are exempt of tax after 30 years. On the other hand, this does not justify - purely financially - buying your main residence in Geneva, since the annual additional cost in other taxes is easily in excess of 50k-.

Sources

In Schwyz, a link to an xls for tax calculation can be found on this page: the portion of capital gains above 40k- is taxed at 30%, with a time-dependent allowance of up to 70%, which means a rate of 9% on large capital gains over 25 years.

In Zug, a link to calculation rules can be found on this page: the rate has starts at 10% and has a maximum that depends on the holding period (between 60% and 25%). In reality, it is often the minimum of 10% that is applicable, since the default rate is the annual yield = capital gain/initial amount/number of years, which is usually less than 10%.

In Zurich, applicable tax rates and calculation examples can be found on this page: the portion of capital gains above 100k- is taxed at 40%, with a time-dependent allowance of up to 50%, meaning a rate of 20% on very large capital gains over 20 years.

In Geneva, the applicable rates are shown on this page and depend solely on the holding period: between 50% and 2%. For 5, 10, 15 and 25%, the rates are 30%, 10%, 10% and 2% respectively.

2nd pillar and 3rd pillar withdrawal

Each household is taxed according to the total amount of 2nd and 3rd pillar withdrawals in that year.

In general, each account can only be withdrawn in full, and only around retirement age.

The tax varies according to the municipality, and is progressive according to the amount withdrawn.

A calculator is provided by Credit Suisse on this page and allows you to simulate the following cases.

3rd pillar withdrawal

The amounts from 50k- to 500k- correspond to realistic scenarios for 3rd pillar withdrawal, depending on whether you have created several accounts (which you can withdraw separately).

2nd pillar withdrawal

The amounts from 200k- to 2m- correspond to realistic amounts for withdrawals from the 2nd pillar, which can generally only be made in one lump sum at retirement.

Höfe (SZ) is still the winner, even if less so as amounts increase: this is due to the high progressivity of tax in the canton of SZ.

Inheritance tax

It's not a criteria: it's zero for the 4 places.

Inheritance or gift tax towards children exists only for the cantons of LU, NE, VD, AI. You'll find more details here and also about donations to others.

About the author

Hello, you can call me Margot.

I'm a French expatriate living in Switzerland. I've been investing for 15 years.

With assets in the low millions, I'll probably never have a family office, so I have to stay in the driving seat. How can I grow my assets further and pass them on to my children?

AskMargot is my testimonial, that of a peer, to go further in wealth management.

You'll find unique content, more advanced than what you'll find on beginner investment blogs or in the wealth reports of French or Swiss asset managers.

Don't hesitate to contact me if you'd like to discuss your wealth strategy with a peer.

Recent articles for Swiss residents